Servo motors are integral to industrial automation, medical devices, and automobiles, offering precise motion control. The global market is set for steady growth from 2025 to 2030, driven by advancements in automation, robotics, and electric vehicles (EVs). This report provides insights into global and U.S. market trends, key manufacturers, revenue projections, and supply chain factors, including raw materials sourced from China and Canada.

Global Market Outlook (2025–2030)

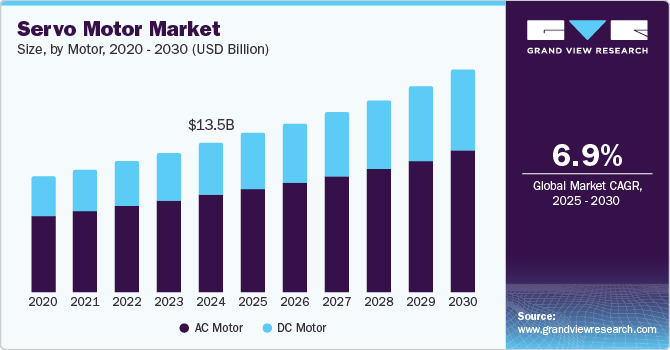

The global servo motor market is projected to grow from $13.5 billion in 2024 to approximately $20.1 billion by 2030, reflecting a CAGR of 5.5–7%. This expansion is fueled by increasing investments in automated manufacturing, smart factories, and AI-driven robotics.

Asia-Pacific leads the market, accounting for 47.8% of global revenues in 2024, with China representing around 22% due to its dominant position in robotics, electronics, and EV production. North America and Europe remain significant markets, with demand driven by industrial automation, aerospace, and healthcare applications.

The rise of EV production, automated logistics, and intelligent manufacturing systems will further increase servo motor adoption globally. Growth in smart factories and AI-powered production lines will sustain demand throughout the forecast period.

Source: Grand View Research – Servo Motor Market Size & Trends, 2025 – 2030

U.S. Market Focus

The U.S. servo motor market is expected to reach $4.1 billion by 2030, growing at 4.0% CAGR. The primary driver is the adoption of smart automation across industries, particularly in robotics, precision manufacturing, and aerospace.

Key sectors contributing to demand include:

- Industrial Automation – Servo motors are widely used in robotic assembly lines, CNC machining, and warehouse automation systems.

- Automotive – The shift toward EV production and autonomous vehicles is driving demand for high-precision servo motors.

- Aerospace & Defense – Increased use of servo-controlled actuators in flight control systems, drones, and defense robotics.

The U.S. government’s focus on domestic manufacturing and AI-powered automation is accelerating investments in advanced servo-driven systems. However, labor shortages and the need for higher efficiency are the biggest contributors to the increasing adoption of automation.

Source: KBV Research – US Servo Motors Market Size, Share & Trends Analysis Report, 2023 – 2030

Key Industry Segments: Industrial, Automotive, and Medical Applications

1. Industrial Automation (Manufacturing & Robotics)

Industrial automation remains the largest segment for servo motors, accounting for over 60% of global revenue. Servos play a crucial role in:

- Robotic arms in assembly lines

- CNC machines for precision machining

- Automated packaging and semiconductor production

The adoption of Industry 4.0 and smart factories is increasing demand for servo-driven robotic automation, with manufacturers integrating IoT-enabled motion control for greater efficiency.

Source: Allied Market Research – Servo Motors Market Overview

2. Automotive Industry

The automotive sector is a major consumer of servo motors, primarily for:

- Robotic welding, painting, and assembly lines

- Battery and drivetrain manufacturing in EV production

- Precision machining for advanced vehicle components

With the transition to EV production, manufacturers are investing in automation for battery pack assembly and high-precision manufacturing. Servo motors are also increasingly integrated within vehicles, particularly in power steering, braking systems, and advanced driver-assistance systems (ADAS).

Source: Strategic Market Research – Servo Motors in Automotive Industry, 2024–2030

3. Medical Devices & Healthcare Automation

Servo motors are critical in high-precision medical applications, such as:

- Surgical robotics (e.g., robotic-assisted surgeries)

- Imaging systems (MRI, CT scans)

- Motorized prosthetics and assistive devices

The aging population and increasing demand for minimally invasive procedures are fueling the adoption of servo-driven medical robotics. By 2030, the medical servo motor market is expected to reach $3.1 billion, growing at a CAGR of 5%.

Source: Valuates Reports – Medical Surgical Robot Servo Motors Market, 2022–2029

Market Share and Key Manufacturers

The servo motor industry is highly fragmented, with the top three companies holding about 25% market share. Major global manufacturers include:

- Yaskawa Electric (Japan) – Leading provider of industrial motion control systems

- Mitsubishi Electric (Japan) – Strong presence in automation and robotics

- Siemens AG (Germany) – Focused on factory automation and smart servo solutions

- Fanuc Corporation (Japan) – Major supplier of robotic servo motors

- ABB Group (Switzerland) – Leading industrial motion control manufacturer

- Rockwell Automation (U.S.) – Major U.S. supplier for industrial servo systems

- Bosch Rexroth (Germany) – Serves the automotive and manufacturing sectors

Source: Allied Market Research – Competitive Analysis: Major Global Players

Supply Chain & Material Sourcing: China and Canada

1. Rare Earth Dependence (China)

Most servo motors rely on rare earth magnets, primarily neodymium and dysprosium, which are predominantly sourced from China. China controls 85–90% of global rare earth supply, making the industry vulnerable to supply chain disruptions and price volatility.

Past export restrictions from China have led to price spikes, highlighting the risks of dependence on a single supply region. In response, manufacturers are exploring:

- Alternative motor designs using ferrite-based magnets

- Supply diversification strategies

- Stockpiling critical raw materials

Source: Reuters – China’s Rare Earth Supply Chain Monopoly

2. Canadian Supply Chain Initiatives

Canada is actively working to reduce dependence on Chinese rare earths by developing its own mining and processing facilities. The Saskatchewan Research Council is building a rare earth processing plant, expected to supply North American manufacturers starting in 2025.

Additionally, Canada remains an important supplier of aluminum and nickel, which are used in motor housings and electrical conductors. Strengthened U.S.-Canada trade agreements are expected to ensure stable access to these resources.

Source: St. Albert Gazette (Canadian Press) – Canada’s Rare Earth Processing Initiatives

3. Trade Regulations & Price Fluctuations

- U.S.-China tariffs (2018–2019) increased servo motor component costs by 10–25%

- Steel and aluminum tariffs disrupted North American supply chains

- Copper and semiconductor shortages (2021–2022) led to price spikes and lead time issues

These disruptions have led manufacturers to diversify their supplier base and increase North American and European sourcing to mitigate risks.

Source: Peterson Institute – US-China Tariffs Timeline

Conclusion

The servo motor market is expected to experience steady growth through 2030, driven by:

- Industrial automation and smart manufacturing adoption

- Expansion of EV production and automotive automation

- Robotic and AI-driven healthcare applications

The U.S. market is projected to reach $4.1 billion, with Asia-Pacific maintaining dominance in global sales. Supply chain resilience and raw material sourcing will continue to shape industry trends, with a focus on reducing dependency on China.

Companies investing in next-generation servo technology, AI-driven control systems, and supply chain diversification will be best positioned for success in this evolving market.